- Status

- Draft regulation of the European Commission

- Status

- Last update

- Legal nature

- Planned optional European private company

- Political framework

- 28th Regime

- Key objectives

- Digital incorporation in 48 hours, under €100, without minimum share capital

- Already applicable law?

- No. The draft is currently in the ordinary legislative procedure.

- Names

- EU Inc., S.EU (Single European Company)

EU Inc., also referred to as S.EU, is the proposal for an optional European private company within the so-called 28th Regime. The European Commission submitted the draft regulation on . The legal form has not yet been adopted; the draft is currently in the ordinary legislative procedure.

Editorial note on the status: This page describes the 28th Regime based on the draft regulation by the European Commission of 18 March 2026 and the parliamentary resolution of 20 January 2026. The draft is currently in the ordinary legislative procedure. All legal statements that are based on law that has not yet been adopted are phrased in the conditional mood. This text does not replace legal advice.

- On 18 March 2026, the European Commission officially submitted the draft regulation for EU Inc. (28th Regime).1

- Core promise: company incorporation in 48 hours, fully digital, under €100 in costs, no minimum share capital.

- The legal form is optional—SE and other national forms will continue to exist unchanged.

- S.EU (Single European Company) is the term used in the parliamentary resolution; the Commission introduced the term EU Inc. Both refer to the same initiative.

- Tax law, insolvency law and employment law remain regulated at the national level; the applicable law of the register seat applies.

- Goal: agreement between the European Parliament and the Council by the end of 2026; likely applicability from the end of 2027 or 2028.

What is EU Inc. / S.EU? Definition and legal classification

EU Inc. – officially Societas Europaea Incorporata, also referred to in German as the Single European Company (S.EU) – is a planned optional company form based on an EU regulation. It is intended not to replace the existing company law of the 27 Member States, but to complement it with a uniform set of rules that companies can choose as an alternative to national legal forms.2

At its core, it is a limited-liability company that is fully anchored at the supranational level: once registered, the same rulebook applies for EU Inc. regardless of which Member State the seat is chosen in. In political documents, this concept is often described as a “virtual 28th Member State”—an image that captures the functional logic without implying a geographically identifiable place.3

Technically and legally, according to the Commission’s proposal it is an EU regulation based on the EU’s internal market competence under the TFEU. A regulation applies in all Member States directly, without national transposition acts. This fundamentally differs from a directive, which would have produced 27 national implementing laws—and thus 27 potential deviations.

“Europe has the talent, the ideas and the ambition to become the best place for innovators. But today, European entrepreneurs who want to expand face 27 legal systems and more than 60 separate company forms at the national level. With EU Inc., we make it drastically easier to found and scale a company across Europe.”

European Commission President Ursula von der Leyen, press release of the European Commission, 18 March 2026

Why now? The political background

The initiative is not a spontaneous impulse, but the result of a multi-year process of discussion based on two influential reports: the Internal Market report by Enrico Letta (April 2024) and the Competitiveness report by Mario Draghi (September 2024). Both reports identified the fragmentation of European company law as a structural disadvantage in global competition.4

Specifically: European founders who want to operate in multiple EU countries navigate through 27 different register procedures, capital requirements, standards for articles of association, and sometimes different languages. While a US company can access the entire US market with a single Delaware incorporation, its European counterpart often fails already at the differing requirements of the first two or three target markets.5

For years, start-up associations and growth companies (scale-ups) have been calling for a “European super legal form.” The informal working title “EU Inc.” was already used in the start-up scene before it took on an official character. The European Commission picked up on this demand and embedded the plan in its start-up and scale-up strategy.

Chronology: From the initiative report to the Commission proposal

The core elements of the draft regulation (18 March 2026)

The Commission’s draft translates the political intent into legally tangible cornerstones. Below are the key elements as they emerge from the draft and the accompanying Commission documents. Since this is a draft that has not yet been adopted, changes during the legislative process are possible.

Incorporation and registration

The incorporation of an EU Inc. is intended to be fully possible digitally and to be completed within 48 hours—counted from the time complete documents are submitted. Costs are intended to be under €100. No minimum share capital is planned. Founders should be able to choose the registration country freely within the EU, which means competition between registration locations.1,3

In addition, the Commission plans to introduce the so-called European Business Wallet—a digital identity and document portfolio with which company data only needs to be stored once across the EU. This should eliminate the need to apply again for tax and VAT identification numbers.3

Scope and legal form

Contrary to earlier drafts and the parliamentary resolution, the Commission’s draft states that, in principle, EU Inc. should be open to all companies—regardless of size. The original restriction to non-listed companies was retained in the parliamentary approach; whether and how this appears in the final legal act is the subject of ongoing negotiations.6

Corporate governance and capital structure

Shareholders should be able to choose flexible capital participation structures, including a separation of voting rights and property rights. This is intended in particular to facilitate venture capital financing, in which investors often require specific liquidation preferences or anti-dilution clauses. For employee participation programmes (ESOPs), the draft provides for a uniform, deferred taxation across Europe upon sale of shares.3

Employee involvement and employment law

For new incorporations, the employee involvement right of the respective registration country should apply. The draft does not provide for new, uniform European employee involvement rules. National thresholds for employee involvement should continue to apply once the relevant employment figures are reached. Trade unions—including ver.di and the European Trade Union Confederation (ETUC)—nevertheless criticize the draft as insufficient, as it leaves room to circumvent national employee involvement rules.7

Dispute resolution and jurisdiction

The Commission has asked Member States to set up specialized courts for EU Inc. disputes. Proceedings should also be able to be conducted in English—an offer to international investors and founders who do not have German or local language skills.

Digital operations and liquidation

All company processes—general meetings, transfer of shares, capital increases, communication with authorities—should run digitally by default. Liquidation proceedings should also be fully digitized and simplified. Innovative start-ups should gain access to accelerated insolvency proceedings.3

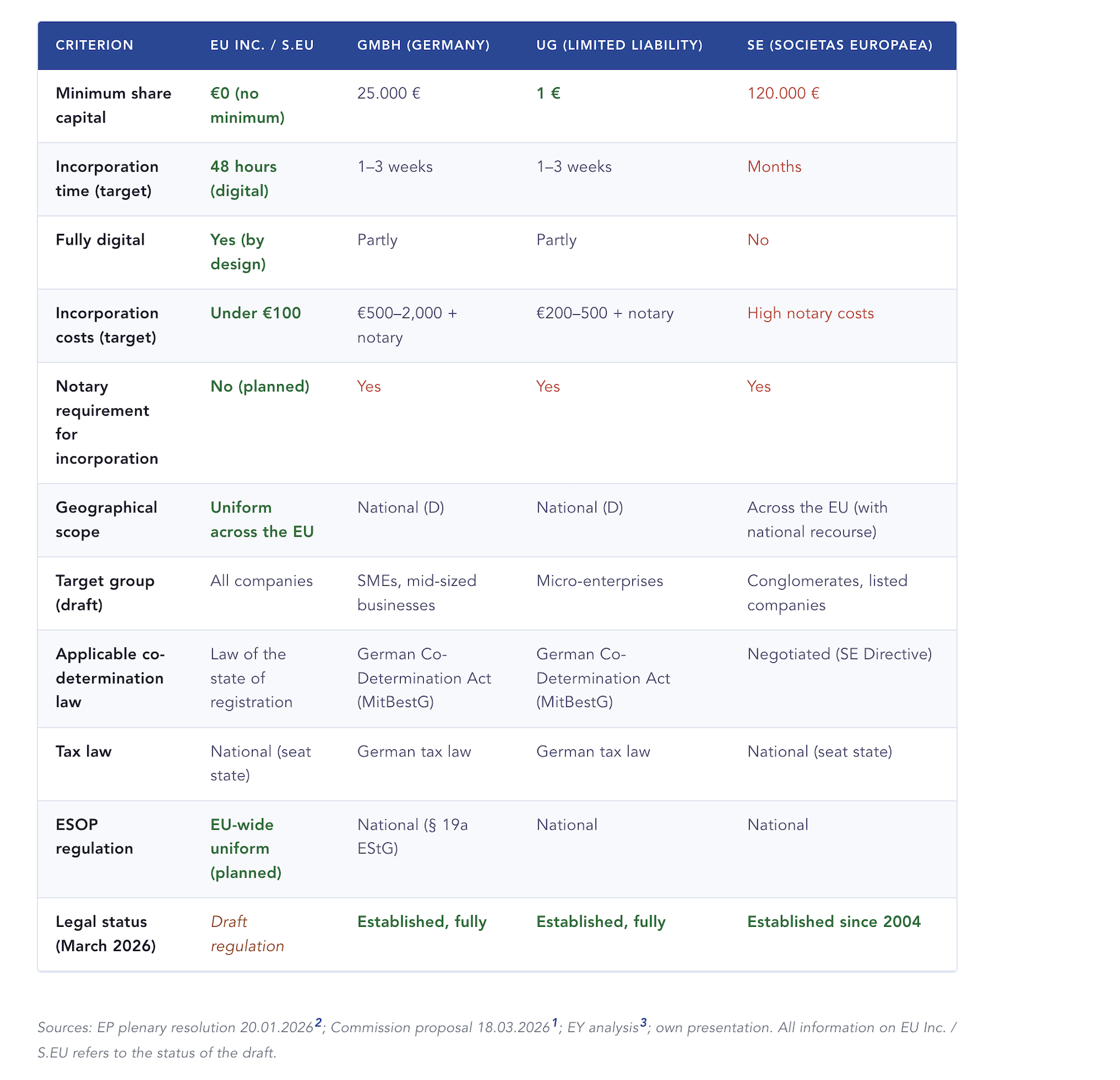

Comparison: EU Inc. / S.EU, GmbH, UG and SE at a glance

| Criterion | EU Inc. / S.EU | GmbH (Germany) | UG (limited liability) | SE (Societas Europaea) |

|---|---|---|---|---|

| Minimum share capital | €0 (no minimum) | 25.000 € | 1 € | 120.000 € |

| Incorporation time (target) | 48 hours (digital) | 1–3 weeks | 1–3 weeks | Months |

| Fully digital | Yes (by design) | Partly | Partly | No |

| Incorporation costs (target) | Under €100 | €500–€2,000 + notary | €200–€500 + notary | High notary costs |

| Notary requirement at incorporation | No (planned) | Yes | Yes | Yes |

| Geographical scope | Uniform across the EU | National (D) | National (D) | Across the EU (with national recourse) |

| Target group (draft) | All companies | SMEs, mid-sized businesses | Micro-enterprises | Conglomerates, publicly listed companies |

| Applicable co-determination law | Law of the state of registration | German Co-Determination Act (MitBestG) | German Co-Determination Act (MitBestG) | Negotiated (SE directive) |

| Tax law | National (seat state) | German tax law | German tax law | National (seat state) |

| ESOP regulation | Uniform across the EU (planned) | National (§ 19a EStG) | National | National |

| Legal status (March 2026) | Draft regulation | Established, fully | Established, fully | Established since 2004 |

Sources: EP plenary resolution 20.01.20262; Commission proposal 18.03.20261; EY analysis3; own presentation. All information on EU Inc. / S.EU refers to the draft status.

Clarification: What EU Inc. is not

EU Inc. is not the SE (Societas Europaea)

The Societas Europaea has existed since 2004 and is the only paneuropean corporate form established so far. It is aimed at publicly listed or large companies and requires minimum capital of €120,000. Incorporation generally requires a conversion from an existing national company. By contrast, the EU Inc. is intended to be possible to set up from scratch—without a predecessor company, without minimum capital, and without a notary requirement. The SE remains in place; it is not replaced by the EU Inc.

EU Inc. is not the failed SPE

Between 2008 and 2014, the EU discussed a Societas Privata Europaea (SPE)—a European private company for SMEs. The proposal failed due to resistance from individual member states, particularly regarding co-determination. The 28th regime is the political successor to this project, with a revised approach and a different legislative route.

S.EU and EU Inc. mean the same thing

S.EU (Unified European Company / Societas Europaea Unica) is the name used by the European Parliament in its resolution of 20 January 2026.2 In its draft regulation, the European Commission refers to EU Inc. In practice and in media reporting, both terms are used synonymously. In addition, the abbreviation “28th regime” is also used as the name for the overarching political project.

Practical relevance for founders and companies

If the EU Inc. were to enter into force in the intended form, different company types would have different levels of relevance.

For startups and scale-ups with European growth plans, the benefit would be most immediate: a single corporate document, a single register, a uniform legal framework for investor agreements and ESOPs—rather than the current need to restructure in each expansion country. Especially in international venture capital rounds where US or UK investors work with standardized contract templates, the EU Inc. could lead to significant simplification.

For established mid-sized businesses that have so far operated with a German GmbH, the EU Inc. would not initially be a mandatory alternative. However, it could become interesting for companies planning subsidiary incorporations in multiple EU countries or that want to simplify the existing holding structure. Whether a simple change of form from the GmbH to the EU Inc. will be possible is not yet conclusively regulated in the draft.8

For international companies outside the EU that want to establish a European entity, the EU Inc. could be particularly attractive: no forced “home-state bias,” free choice of location, uniform contract law. The question of which member state offers the most attractive registration environment (lowest costs, fastest authorities, most favorable tax law) will likely become a new competitive factor between member states.

Risks, limits, and critical voices

Trade unions: risk to co-determination

ver.di described the draft as a “gateway for weakening employees’ rights.” The European Trade Union Confederation (ETUC) called for revision so that clear statutory provisions would ensure that the Commission’s stated intention—no impairment of employees’ rights—is actually implemented.7 Key point: Because the co-determination regime is linked to the place of registration, companies could choose a seat in member states with lower co-determination thresholds in order to avoid German or Austrian co-determination rules.

Notaries and company registry lawyers: risks regarding minimum capital and the 48-hour deadline

The Federal Chamber of Notaries (Bundesnotarkammer) warns in a detailed statement about the risks of a minimum subscribed capital of one euro. A regulatory competition downward (“race to the bottom”) could permanently damage trust in the new legal form. The 48-hour deadline should also be viewed critically if it includes the advisory phase before the actual filing—such an interpretation would hardly be compatible with an appropriate level of quality and security.7

Missing supranational institutions

Several expert voices criticize that the draft does not provide for a uniform European commercial register or a clear supranational judicial jurisdiction for disputes involving EU Inc. References to national law in central areas such as insolvency law and tax law weaken the intended uniformity.8

Ambitious timeline

The Commission has set the goal of completing the legislative process by the end of 2026. Experts consider this timeline very ambitious, especially given the complexity of the disputed issues (co-determination, tax, registry structure). If agreement is delayed, the practical availability of the EU Inc. would correspondingly shift.

Common misconceptions about the EU Inc.

The EU Inc. is already available and can be used now.

The draft regulation was submitted on 18 March 2026. Before the legal form can be used, Parliament and the Council must adopt the draft. Even with a fast legislative process, practical availability is realistically at the earliest at the end of 2027 or 2028.

The EU Inc. makes GmbH, UG, and SE unnecessary.

The EU Inc. is designed as an optional addition, not a replacement. All 27 national legal systems remain fully in place. For companies with purely national activities, the GmbH or UG will continue to be the more obvious choice.

With the EU Inc., you can optimize taxes because you can freely choose the tax law.

Tax law is explicitly regulated nationally in the draft. The law of the state where the seat is located applies. The EU Inc. does not create special tax rules and does not replace existing national tax obligations.

S.EU and EU Inc. are different legal projects.

Both terms refer to the same initiative. S.EU is the short form of the EP resolution from January 2026; EU Inc. is the name used by the Commission in the draft from March 2026. In the public sphere and among professionals, both terms are used synonymously.

Decision aid: For whom is the EU Inc. potentially relevant?

| Type of company | Relevance of the EU Inc. | Recommendation today |

|---|---|---|

| Startup with EU expansion (Seed / Series A) | High | Monitor developments; think ahead about an EU-friendly structure now. |

| Scale-up with activities in 3+ EU countries | Very high | Detailed review of the draft; if necessary, check the existing holding structure. |

| Mid-sized business with purely German market | Low | Wait and see; the GmbH remains the first choice. |

| International company (non-EU) with access to the EU market | High | Develop a registration location strategy early. |

| Group with SE structure | Medium | The SE remains sensible; the EU Inc. could be interesting for subsidiaries. |

| Individual founder / micro-enterprise (national) | Low to medium | Keeping the UG or GmbH is simpler and immediately available. |

Own assessment based on the Commission draft of 18.03.2026. Not to be understood as legal advice.

Practical example

TechVenture GmbH expands to France, Poland and the Netherlands

The TechVenture GmbH from Munich has 18 employees and operates a B2B software platform. So far, it has been active exclusively in Germany. Now the company plans to enter three new markets at the same time.

Under current law, TechVenture would have to set up a SARL in France, a sp. z o.o. in Poland and a B.V. in the Netherlands—each with local notaries, local company registration law and its own articles of association standards. This would also involve separate bank accounts, separate ESOP structures and compliance costs in three jurisdictions.

With an EU Inc. (once available), TechVenture could instead set up a single EU Inc.—with a registered office of its choice, a single set of articles of association and legal personality valid across the EU. Local tax registrations would still be required; however, the corporate-law effort for the expansion would be significantly reduced.

Media

Frequently asked questions (FAQ)

Not yet. The draft regulation was submitted on March 18, 2026. It is now going through the EU’s ordinary legislative procedure (Parliament and Council). According to the current schedule, the earliest practical availability would be at the end of 2027 or during 2028—provided that an agreement is reached by the end of 2026.

None: Both terms refer to the same initiative. S.EU is the abbreviation of the parliamentary resolution from January 2026; EU Inc. is the name used by the Commission in the draft regulation from March 2026. In the press and among industry experts, they are used synonymously.

No. The EU Inc. is designed as an optional addition. All national legal forms—GmbH, UG, AG and others—remain fully in place. Companies can choose whether they want to use the EU Inc.; there is no obligation.

According to the Commission’s draft, the formation should be notary-free and fully possible digitally. However, this is a politically sensitive point that is still being negotiated during the legislative process, since in several member states (including Germany and Austria) notaries play a legally established role in company formations.

Tax law depends on the law of the state of its registered seat. The EU Inc. does not create a special tax status of its own. Corporate income tax, VAT, and other national tax obligations remain unaffected.

This question has not yet been answered conclusively in the current draft. Some experts in business law explicitly call for the possibility of a simple change of legal form. Whether and under what conditions a switch will be possible depends on the final text of the law.

The 28th regime is the political term for the overall package: a single, uniform rulebook applicable across the EU for companies, which sits alongside the 27 national legal systems—hence “28”. EU Inc. and S.EU are the specific company forms that are intended to be created within this framework.

The SE has existed since 2004, requires minimum share capital of €120,000, and is primarily aimed at large, often publicly listed companies. Formation generally requires a conversion from a national company. The EU Inc., by contrast, is intended to be founded from scratch, without minimum capital, digitally, and within 48 hours—and it is explicitly also aimed at SMEs and start-ups.

Sources and further documents

Footnotes

- European Commission, press release, 18.03.2026: commission.europa.eu – EU Inc. Making Business Easier

- European Parliament, press release REF 20260116IPR32438, 20.01.2026, voting result 492:144:28.

- EY Germany, tax-law analysis of the Commission proposal, March 2026: Regulation enters into force 20 days after publication in the EU Official Journal; applicable 12 months thereafter.

- Draghi report: “The Future of European Competitiveness”, September 2024; Letta report: “Much More than a Market”, April 2024.

- EP Research Service: “Identifying obstacles faced by companies, especially innovative start-ups, in the EU” (IUST_STU(2025)775947), 2025.

- In the Commission draft of 18.03.2026, the scope has been expanded to all companies; the EP resolution had limited it to non-listed capital companies.

- ver.di press release of 18.03.2026; EGB press release (English) of 18.03.2026; Federal Chamber of Notaries, statement 2025/2079(INL).

- Speedinvest, Austrian Chamber of Notaries, Brutkasten: Reactions to EU Inc., 18.03.2026.